How an AI Company in Japan Gained $2.5bn and Lost It All in 6 months

Learnings from the Rise and Crash of an AI Sensation in Japan

Learnings from the Rise and Crash of an AI Sensation in Japan

Once in a while, a sensational company makes headlines with a revolutionary product or business model.

In Japan, that company was “AI Inside,” an AI OCR company that went public on 2019/12 on the Tokyo Stock Exchange Mothers (startup-focused) Index.

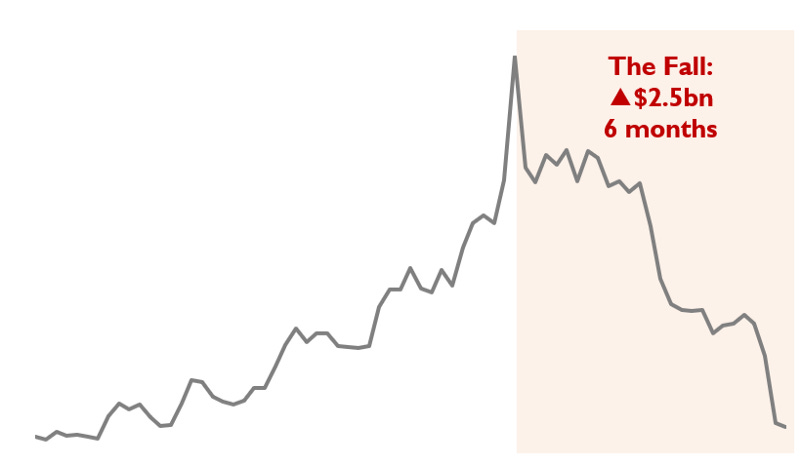

After an opening price of $120, it had a sensational run to a price of $900 (~7x) in a matter of 11 months. Its first fiscal year had 350% revenue growth.

Business newspapers, venture capitalists, and the start-up community all couldn’t stop talking about the company. Personally, currently working in an AI Startup in Japan, I was amazed and envious of their massive growth and success.

Introduction: What is AI Inside?

AI Inside is an AI startup established in 2015 by a CEO with a background as an AI Engineer. He is a serial entrepreneur who has built and divested multiple companies before founding AI Inside.

In college, he wrote a 200-year timeline of important events to happen during 1900–2100. From this exercise, he concluded that “Space” and “AI” will be the key technologies of our future and decided to focus on AI due to the expensive upfront investments required in space technology.

In AI Inside, he focused on the technology of OCR (Optical Character Recognition). AI Inside built a SaaS product called “DX Suite” that converts handwritten invoices and documents into digital data with considerably high accuracy (~99.9% or more).

The product is an excellent fit for the Japanese market, where a vast amount of human labor still converts handwritten documents manually.

The Rise: Sensational Run Upwards

The “DX Suite” product was a massive success in Japan. Their products were selling like hotcakes. Just take a look at the stats for yourself.

・ An ARR (Annual Recurring Revenue) growth rate of 208.6%, which is astounding even in high-growth SaaS companies.

・64% market share in the OCR Market, with over 36,000 licenses.

・Two upward revisions in revenue guidance in the same Fiscal Year. (Initial estimate: $26.3M, 1st Upward Revision: $35.8M, 2nd Upward Revision: $44.7M)

・An operating profitability margin of 41.6%,

You can imagine the excitement of investors upon hearing this news amidst the pandemic. A company that is growing at 200%+, with a profit margin of 40%+? Insane!

For some context, Snowflake (a high growing SaaS) company is growing at around 80%, but at an operating loss. Salesforce (later stage SaaS) is growing at around 20%+ with a margin of 20%+, which is considered extremely impressive.

As a result, AI Inside had a massive bull run, gaining a market cap of +$2.5bn within eleven months. Hence, AI Inside became the darling of tech startups in Japan.

AI Inside accomplished this high growth, high margin business model using an unconventional strategy in the SaaS industry.

Full Leverage of Partner Sales (~90% of sales): After building a viable product in 2018, AI Inside decided to sell using partnerships primarily. They have about 100 partners, ranging from a sales partner to an OEM partner. Their partnership strategy allowed AI Inside to reduce their sales staff and advertising budget.

Slashing Prices to Increase Market Share: They initially had a DX Suite Standard price model with a $2,000 Initial Fee and a $10 Monthly Fee, but they decided to add a much cheaper product lineup to get market share from SMBs and government entities in Japan. It had a free Initial Fee with a $3 Monthly Fee. You can guess that the Lite Plan was a hit, with 11,957 new contracts in 2020.

Building their own Data Centers for Product Deployment: AI Inside decided to steer away from public cloud servers to reduce their costs.

Until recently, AI Inside was seen as a market disruptor with a revolutionary business model and a high-quality product. However, this all changed soon after.

The Fall: The Massive Run Down

Suddenly without any advanced notice, AI Inside released an ominous press release on 04/28/2021.

The note mentioned that one of their OEM partners, NTT West, will not renew 80% of their contracts in the next fiscal year. More surprisingly, NTT West contributed about $21M of revenue to AI Inside, about 50% of their total revenue. Shockingly, this meant that a vast chunk of AI Insides revenue would be erased next year.

You can imagine this news scared off investors with a lot of unanswered questions.

“How would AI Inside compensate for the lost $17M in revenue?”

“Does this mean their product has a critical issue?”

“Are there risks associated with other partnerships?”

Without any further explanation from AI Inside, investors massively sold the stock 3~4 days in a row, reaching the maximum limit of a single-day loss every single day.

The next time we heard from AI Inside regarding the matter was on 05/12 during their Q1 earnings. The earnings statement worsened the situation. The forward revenue guidance was 20% lower than this year's revenue, and the profit margin decreased 80%. Investors were devastated (and still are).

Final Thoughts

I believe AI Inside’s initial success and the eventual decline have plenty of learnings for new startups utilizing emerging technology.

Great Product and Use Case: One of the pitfalls of an emerging tech startup is the excessive focus on the newest algorithm with the highest accuracy. What is more important is the user experience and whether the product solves the issue of the client. In most cases, you may not need the latest algorithm. AI Inside was one of the first AI companies in Japan with a scalable product. For this reason, their successful product serves as a benchmark for emerging AI companies.

The Pitfalls of Rapid Expansion: Although the exponential growth of AI Inside was impressive, the main issue lay in AI Inside’s inability to lead their clients to customer success. They offered too many products to too many customers and relied heavily on partners to renew contracts. There is a reason why SaaS companies still invest a considerable amount in ensuring customer satisfaction and success. You cannot expect your partners to renew customer contracts when there are still many iterations in the product.

Importance of a Clear Growth and IR strategy: It is fair to say that AI Inside’s IR strategy is one big reason why the stock price has taken huge turns. People are wondering, didn’t AI Inside know about this risk of NTT West’s contract expiration earlier than 04/28? Why wait to tell the public only after the stock price was so vastly inflated? Also, did AI Inside need to revise their guidance twice in the fiscal year to largely raise expectations? If AI Inside decided to stick to a normal revenue growth trajectory, the stock price would have taken a different route. Not surprisingly, the CEO had sold a large number of shares before the share price plummeted to its current levels.

Overall, AI Inside reiterates that they are bullish about the long-term growth of their product and that this development with NTT West was a one-off event.

“The event with NTT West is a temporary event that does not impact the long-term future of our company.” — CEO, 05.12 Earnings Call

They also have a brewing idea to develop a new platform for non-coders to build AI models within a few clicks. It will be interesting to see what awaits for AI Insides future, but one thing is for sure: It will take a long time until AI Inside regains trust from investors. If AI Inside underperforms in any of their future earnings, the stock price would surely plummet even more.

This event also is a good example for retail investors to learn from. The volatility of the stock demonstrates the dangers of mania associated with “buzzword stocks” tagged with words such as “AI,” “Electric Vehicles,” and “Space.” Although I believe in disruptive technologies, retail investors need to carefully scrutinize the company’s business model, technology, and organization before investing in such companies.